you position:Home > new york stock exchange > new york stock exchange

Stock Options: IFRS vs. US GAAP

![]() myandytime2026-01-17【us stock market today live cha】view

myandytime2026-01-17【us stock market today live cha】view

info:

In the dynamic world of financial reporting, understanding the differences between International Financial Reporting Standards (IFRS) and U.S. Generally Accepted Accounting Principles (US GAAP) is crucial, especially when it comes to stock options. This article delves into the disparities between these two accounting frameworks, highlighting their impact on the recognition, measurement, and disclosure of stock options.

Understanding Stock Options

Stock options are a form of employee compensation that gives employees the right to purchase company shares at a predetermined price, known as the exercise price, within a specified time frame. These options can be a powerful tool for attracting and retaining top talent, but they also present complex accounting challenges.

IFRS vs. US GAAP: Recognition

Under IFRS, stock options are recognized as an expense in the period they are granted, based on their fair value at the grant date. This expense is recognized over the vesting period, which is the period over which the employee must satisfy the conditions to receive the shares.

In contrast, US GAAP requires the recognition of stock options as an expense only if the fair value of the options can be reliably measured. If the fair value cannot be reliably measured, the options are not recognized as an expense.

IFRS vs. US GAAP: Measurement

Both IFRS and US GAAP use the Black-Scholes model to estimate the fair value of stock options. However, there are some differences in the inputs used to calculate the fair value under each framework.

Under IFRS, the volatility of the underlying stock is estimated using a historical volatility approach, while US GAAP requires the use of a market-based volatility estimate. Additionally, IFRS allows for the use of a risk-free rate derived from a government bond yield, whereas US GAAP requires the use of a corporate bond yield.

IFRS vs. US GAAP: Disclosure

Both IFRS and US GAAP require companies to disclose information about their stock option plans, including the number of options granted, the exercise price, and the vesting period. However, IFRS requires more detailed disclosure about the assumptions used to calculate the fair value of the options.

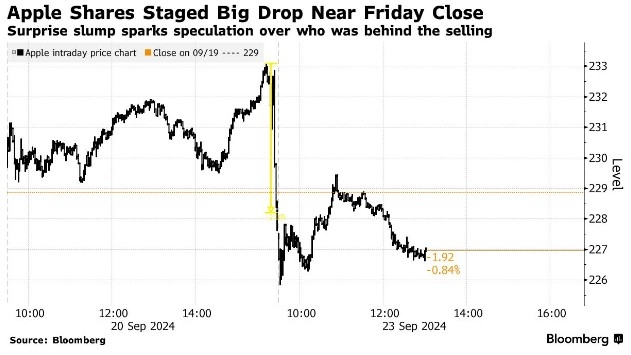

Case Study: Apple Inc.

A notable example of the impact of these differences is seen in the financial reporting of Apple Inc.. Under IFRS, Apple recognized a significant expense related to its stock options in its 2018 financial statements. However, under US GAAP, the expense was much lower, as the fair value of the options could not be reliably measured.

Conclusion

The differences between IFRS and US GAAP in the treatment of stock options can have a significant impact on a company's financial statements. Companies must carefully consider these differences when preparing their financial reports to ensure compliance with the relevant accounting standards and provide accurate and transparent information to investors and stakeholders.

so cool! ()

last:High Dividend US Stocks 2016: Top Investments for Income Seekers

next:nothing

like

- High Dividend US Stocks 2016: Top Investments for Income Seekers

- US Stem Cell Clinic Stock: A Game-Changer in Regenerative Medicine

- How Much Is the US Stock Market Down?

- Understanding US Energy Stocks ETF: A Comprehensive Guide

- Top US Mid Cap Stocks: A Guide to Investment Opportunities

- Title: Top Performing US Stocks Last 5 Trading Days July 2025

- Elekta US Stock: A Comprehensive Analysis

- Is the US Stock Market Closing Early Today? Everything You Need to Know

- Title: "President Trump's Tariff Threats on China Rattle US Stocks&

- ACB US Stock Listing: Everything You Need to Know

- Understanding the Role of Social Security Number in US Stock Exchange Transaction

- Best US 5G Stocks: Your Guide to Investment Opportunities in the Future of Connec

hot stocks

Can I Buy US Stocks with CAD?

Can I Buy US Stocks with CAD?- Title: US Oil Companies Stocks: A Comprehensiv"

- Acronym and Name of US Stock Exchange: Codycro"

- Can I Buy US Stocks with CAD?"

- New Millennium Steel Dynamics: A Deep Dive int"

- Current Margin Debt in the US Stock Market: An"

- Sibanye Stillwater Stock US: A Comprehensive A"

- US Bank vs Wells Fargo Stock: A Comprehensive "

- US Army Christmas Stocking: A Symbol of Holida"

recommend

Stock Options: IFRS vs. US GAAP

RAAS Stock US: A Comprehensive Guide to Unders

Top US Penny Stocks to Buy Now: Your Guide to

Stocks and Shares ISA for US Citizens: A Compr

Amzn Stock: Understanding the US Dollar Value

US Brokers: Unlocking the World of Foreign Sto

Can an NRA Gift Us Stock? Understanding the Po

US Global Jets ETF Stock Price: A Comprehensiv

US Stock Market 2017 Predictions: What to Expe

Trump Us Stocks: How the President's Poli

How to Invest in US Stocks from Europe

tags

-

TomorrowAprilFuturesRareGrowingUnderstaComprehensAllegedLNGExchangAcronymHolCanEssentialGoldClosedCannabisEarthPerExchange20182021IndianfromLo5130150NameTankAlternative4245GalChineseIslandStrategyPivotalDefinitioJonesDelhaizeManyA7IIISchwabCompletionMarCitizensFallEdibleMFCListDidNintendo2ndDaysNon-USBogleheOpenHolidaysBYDDelekSmallPurchaseRiskHighwaySixth-Gener2023LargestFoodTotal2019InsectAholdTimingstodshareShausaveruamerican10010miniliveAvnasdaqSustainaPharmaceCleaFuUnderaverage us stocks games silver etf us stock

like

- LG Chem Stock in US Dollars: A Comprehensive G"

- US Natural Gas Stock Quote: A Comprehensive Gu"

- Title: If US Legalized Marijuana Stocks to Inv"

- US MSO Cannabis Stocks: The Future of Legal Ca"

- Meli Us Stock Price: A Comprehensive Analysis"

- Title: Can Foreigners Invest in the US Stock M"

- First 24-Hour US Stock Exchange Approved: Revo"

- http stocks.us.reuters.com stocks fulldescript"

- Understanding the Role of Social Security Numb"

- Airbus Stock Symbol: US - Everything You Need "